If you have a Solo 401k, you can co-invest funds with your spouse in real estate. A highly valued advantage of a Solo 401k account is that prudent investors can combine the income and long-term growth potential of real estate with the tax benefits of a Solo 401k account. This is an awesome combination that can be taken a step further when spouses combine the buying power of both of their Solo 401k accounts to invest in one or more quality rental properties. There are very important reasons that the Solo 401k is superior to other retirement account options for real estate investing.

Why Use a Solo 401k to Invest in Real Estate?

Importantly, no employer-sponsored 401k plans allows you to directly purchase real estate with your retirement account. Maybe you can use your employer-sponsored 401k plan to buy a REIT. But, you have no control over that investment. And, your employer 401k won’t allow your account to own individual properties. It’s a Solo 401k account that provides the advantage of holding title to real estate.

Some investors withdraw funds or take a loan from their employer-sponsored 401k to buy real estate. Unfortunately, loans and withdrawals do not qualify for the tax advantages of a retirement account.

Another option is to use a self directed IRA to invest in real estate. This does have tax advantages. However, there are still disadvantages compared to a Solo 401k. Consider your self-directed IRA borrowing money to help finance the real estate purchase. Those earnings from the property are subject to unrelated debt financed income (UDFI). You’ll pay capital gains and/or income tax on the earnings generated by the borrowed money. This does not apply to Solo 401k accounts. The full earnings stay in your Solo 401k.

Co-Invest with your Spouse for More Purchasing Power

Another reason investors prefer the Solo 401k over the self directed IRA is the ability to combine retirement funds with your spouse. The Solo 401k allows both spouses to co-invest in real estate in the Solo 401k Trust. They each have a separate account within the 401k Trust. However, the 401k Trust can accept funds from both spouses for the real estate investment.

Self directed IRAs are different because they are two individual accounts. Co-mingling two IRAs among spouses would trigger a prohibited transaction (no partnering with a disqualified person). In a prohibited transaction, the IRS can force both accounts to be liquidated and all taxes to become due.

Example of Combining Spouse’s Solo 401k Investing Power

Real estate, such as a rental house, clearly demonstrates the combined power of spouse’s Solo 401k accounts. You can combine this power in most investments such as cryptocurrency or shares in a private business. What’s different about a rental house is that the Solo 401k would own the entire investment. The house title is in the name of the Solo 401k. Your Solo 401k and you as the manager have full control of the asset.

Inside the Solo 401k trust, each spouse can own an individual portion of the account. Maybe it is a 50/50 split, a 60/40 split, or some other combination. What this means is that good records have to be kept. Earnings are credited to each account as a proportion of the ownership. Also, expenses such as property taxes, repairs, and insurance are paid proportionally.

Spouse Investment Example in the Solo 401k

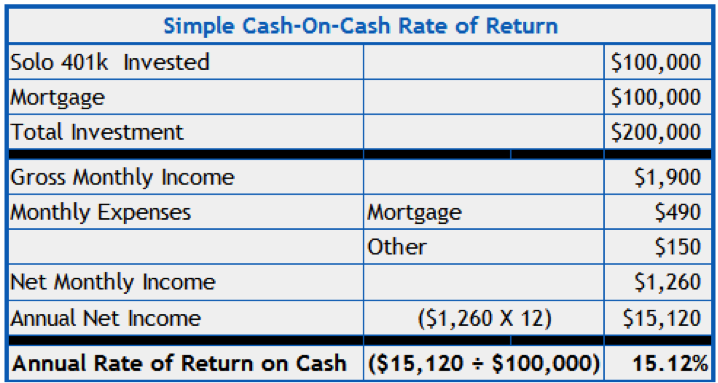

Here is what this type of investment can look like:

- John and Sue open a Solo 401k account for their small business.

- Sue rolls over $70,000 from an old employer-sponsored 401k.

- John rolls over $30,000 from an IRA.

- After thorough due diligence, they select a $200,000 duplex to invest in.

- They fund half the purchase ($100,000) proportionately (70/30) from their Solo 401k Trust.

- The Solo 401k gets a non-recourse 30-year mortgage for the remaining $100,000.

- Interest rates are at historic lows right now but non-recourse loans have a slightly higher interest rate at maybe 4.2%. The monthly mortgage payment will be about $490.

- The 401k collects $950 in rent from each of the duplex units for a monthly total of $1,900.

- Other expenses (taxes, property manager, insurance, etc.) total $150 per month.

- Monthly net income is $1,260 ($1,900 – $490 – $150).

- Proportionately, $882 of earnings goes to Sue’s account each month ($1260 X 70%).

- Proportionately, $378 of earnings goes to John’s account each month ($1260 X 30%).

The total annual cash-on-cash rate of return is a whopping 15.12%.

Follow the Rules When Investing with Your Spouse

Along with the investment flexibility and a high rate of return come a few caveats:

- All rental income must be deposited to the Solo 401k.

- All expenses and costs have to be paid proportionately from each spouse’s Solo 401k account (no personal funds can be used).

- Only a non-recourse loan to the Solo 401k can be used for additional financing (but many loan sources are available).

- Title the property in the Solo 401k name.

- Both Solo 401k underlying accounts must be reconciled, no less than annually and always when processing distributions. Reconciliation should be aligned with the original ratio between the spouses (50/50, 70/30, etc.).

- Always use the Solo 401k name, not personal names.

- Plan owners cannot use Solo 401k investments for personal gain — outside of retirement saving — or to benefit any disqualified person, such as their spouse, parents or children.

- You can use the earnings from one property to finance additional investments in the future.

You Have Options for Initially Funding Your Solo 401k

There are many ways to get started. Here are the most common:

- Rollover or transfer an old employer-sponsored 401k.

- Rollover an IRA.

- Start a new Solo 401k.

- Combine funds from a new Solo 401k with additional funding from an old employer-sponsored 401k or an existing IRA.

Other options include rolling over real estate that is already owned by a self directed IRA into a Solo 401k. You can also use a Roth IRA or Roth 401k. A self directed Brokerage IRA can be the answer for you. Nabers Group is serious about you being in control of your retirement account. We’ll be glad to work with you and your specific circumstances.

Something important to understand is that when you do this, you’ll be rolling over your funds tax and penalty free with the new benefit of being able to use the proceeds to invest in real estate.

Have questions about growing your retirement account? The 401k experts at Nabers Group will help you get your retirement funds into your control, where they belong.