Looking to grow your money aggressively? Consider using investing Roth funds. Roth investments allow your money to grow tax-free. Roth contributions are non-deductible, meaning they use after-tax money. So, while you don’t get the tax deduction on the money going into your retirement plan, you also don’t pay taxes when the money comes out.

Using a Roth Solo 401k can be especially lucrative if you are making an investment you know could skyrocket in value, or if you are able to let the interest on your investment earnings compound over time. In fact, strategically using Roth funds in your Solo 401k could even make you a millionaire.

At first that might sound like hype. Let’s look at how it can become a reality.

High Yield, Asymmetric Investment

If you have an investment you believe can yield a high return, you might want to consider using Roth funds. For example, many investors who used Roth retirement funds to invest in crypto have enjoyed large gains they can eventually withdraw tax free. Similarly, you might consider using Roth funds to make asymmetric bets such as angel investing in start-up companies or a venture capital fund.

If there’s potential for a high return by investing a smaller amount of money up front, Roth might be the way to go.

Investing Over the Long Term

Beyond picking unicorns and other asymmetric bets, how else can investors become a Roth millionaire? The answer, while simple, takes discipline.

Find a good investment with a solid return and wait.

If you can identify an investment with a stable return, over time that investment can grow exponentially. Albert Einstein called this phenomenon the eighth wonder of the world…compound growth.

The Miracle of Compound Growth

Compound growth means you reinvest your earnings, instead of them paying out. This means you’re growing your money, so the return on your growing money is bigger each pay period. This especially makes sense when you are investing with retirement funds, since you won’t take dividends personally anyway. Reinvest the money and let it ride!

Compound growth is especially powerful when you place money over time in an investment with solid returns. Let’s take a look at an example:

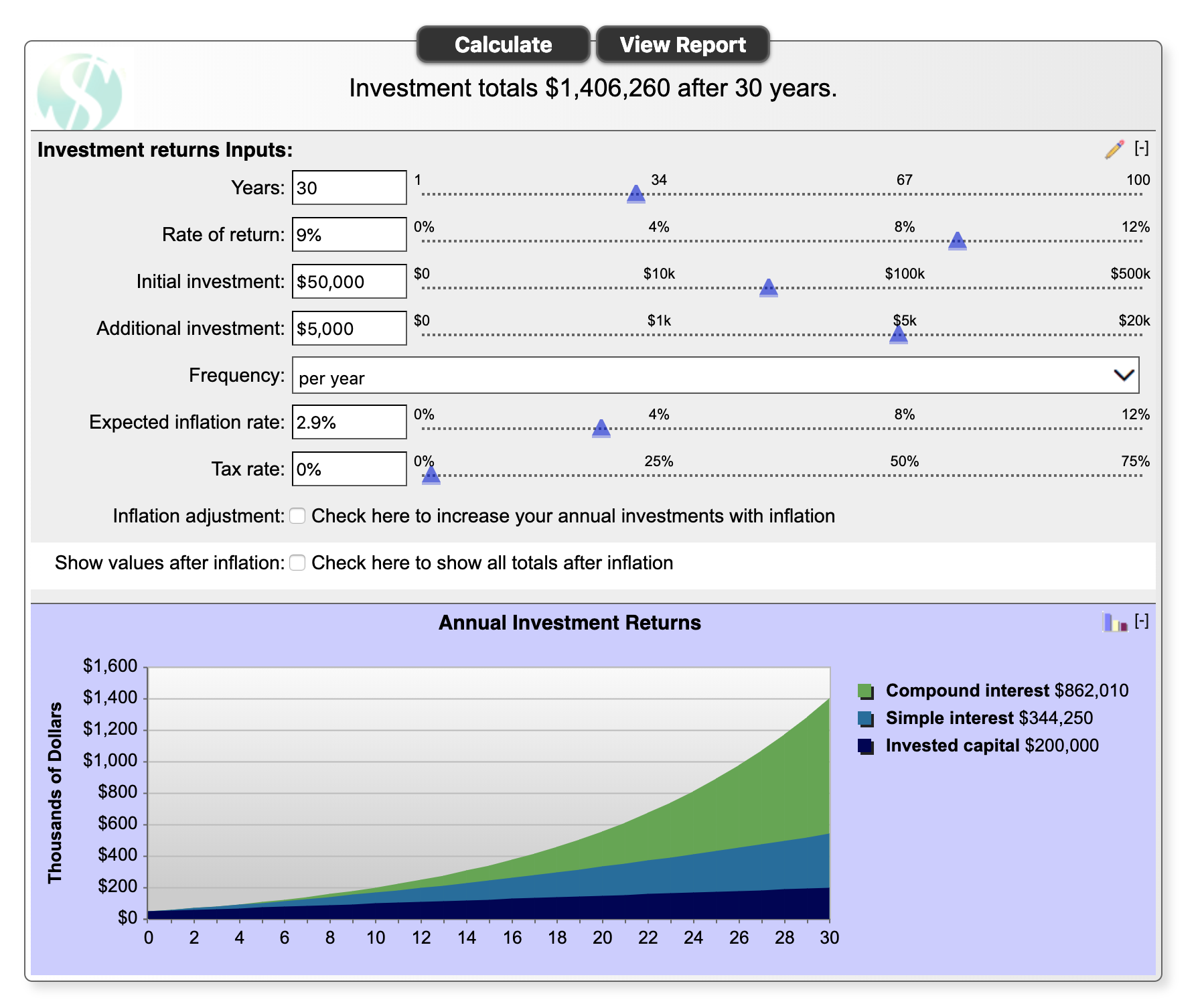

If you are 40 years old, and have a starting portfolio of $50,000, you can still grow to have over a million dollar portfolio in your lifetime. Even if you only put in an additional $5,000 per year, your portfolio can grow by leaps and bounds. By identifying an investment that can yield a 9% annual rate of return, the starting portfolio of $50,000 can grow to $1,406,260 after thirty years.

The bulk of the earnings in the above example is the compound growth on the investment:

- Total invested capital: $200,000 (over 30 years)

- Simple “interest”: $344,250

- Compound “interest”: $862,010

Are you starting with more than $50,000? Can you invest for longer than 30 years? Are you able to get a consistent rate of return in the double digits? Can you put in more than $5,000 per year? Increasing any of those variables could cause you to end up with more money.

Free Resource: Calculate your investment returns here

Why Roth Solo 401k Instead of Roth IRA

Many finance writers tout the magic of the Roth IRA in growing your investments tax-free and they’re not wrong. However, the path to aggressive wealth growth with a Roth Solo 401k can be much faster than growing your wealth in a Roth IRA.

To start, many high earners don’t qualify for the Roth IRA. The Roth Solo 401k has no income ceiling, meaning you can contribute to a Roth Solo 401k, even if you earn “too much” money for a Roth IRA.

With a Roth IRA, you can only invest $6,000 per year (or $7,000 per year if you are age 50 or older).

In a Roth Solo 401k plan, you can contribute $19,000 per year into your Roth 401k account. If you are age 50 or older, that contribution amount increases to $25,000 per year.

If you use the Mega Backdoor Roth strategy, you could contribute up to $62,000 per year after-tax.

Let’s compare a side by side example of Roth IRA versus Roth 401k compound interest and growth:

Roth Solo 401k Returns

The factors in the above example are the same, except for the contribution amount you can put into the Roth retirement plan each year.

Roth IRA:

- Starting age: 30

- Annual Rate of Return: 9%

- Starting Investment: $50,000

- Annual contribution: $6,000 (maximum Roth IRA)

- Investment total after 30 years: $1,554,835

Roth Solo 401k:

- Starting age: 30

- Annual Rate of Return: 9%

- Starting Investment: $50,000

- Annual contribution: $19,000 (maximum Roth Solo 401k)

- Investment total after 30 years: $3,486,313

By investing your Roth funds into a Solo 401k, you could earn $1,931,478 more than with a Roth IRA. What could you do with an extra $1.9 million?

Recap

Retirement account investing can be a lucrative way to grow your nest egg. When you tap into the power of tax-free growth in Roth funds, your wealth can accumulate even faster. Roth investing can be profitable through a high-yield, asymmetric investment, or by capturing the magic of compound growth over the long-term.

When you invest wisely with an eye on the future, you could even use retirement funds investing to make you a Roth millionaire. Are you using Roth funds to invest? Let us know in the comments below.

Disclaimer: Nothing in this post is an offer to transact securities or a guarantee of results, or tax, investment, or legal advice. Any reference to financial performance or return on investment is for illustration purposes only.