Go beyond publicly available REITs and access investment properties directly. You can invest your IRA and 401k funds into houses, condos, land, mortgage notes, and more! Let the gains, rents, any all profits go back into your Solo 401k without taxation. The Solo 401k by Nabers Group gives you the freedom to invest in virtually any real estate deal, whether it be a rental home, a bargain at the foreclosure auction, or a syndicated “insider” real estate development.

The Solo 401k Advantage vs. SDIRA

Avoid the costly “Self-Directed IRA” real estate tax. Many self-directed investors get taxed twice and it eats up most of their profits. Self-Directed IRA custodian accounts and IRA LLC accounts are not designed to be invested in real estate using mortgage financing for leverage and thus are aggressively taxed at the highest rates in the tax code. The Solo 401k solves this because it is exempt from those taxes and that makes it the perfect real estate investing structure. Unlimited® Deal Access + Full Tax Benefits = Maximum Profit For You!

Real World Example

Let’s cover a real world example of the Solo 401k purchasing a piece of real estate. It’s important to use the right sequence of getting your deal done and you must have the Solo 401k established with your plan and trust document to properly title your offer and closing documents.

1) Open Your Solo 401k Account

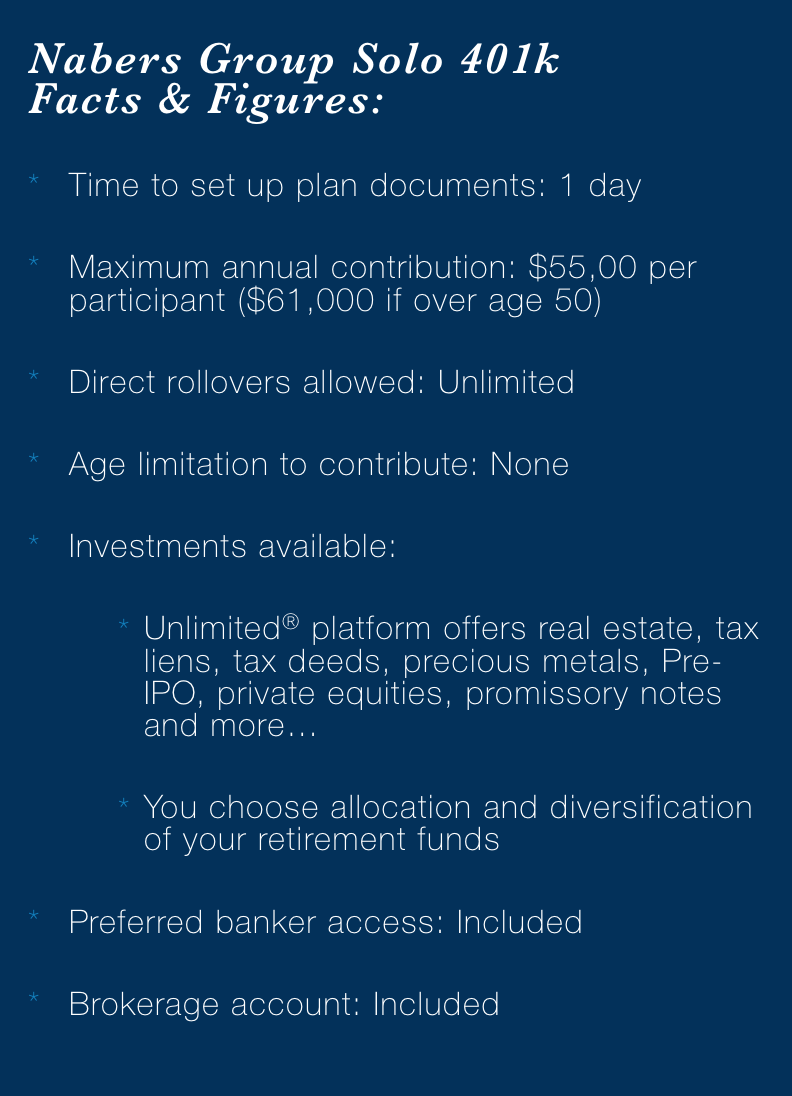

It’s simple and fast to open your Solo 401k with us. Our software platform is the only one of its kind in the world, putting technology to use for you so you can get you plan established in about 1 business day. You’ll have your Solo 401k documents available for download immediately after establishing and have 24/7 access so you can act quickly on great deals without having to wait around for someone to send you paperwork before you can get started.

2) Fund Your Solo 401k

There are a number of ways to quickly and easily fund your Solo 401k. You can roll over funds from existing SDIRA, Solo 401k, traditional IRA, 401k, 403b, TSP (Thrift Savings Plan), Defined Benefit plan or 457b (and more).

You can also fund your plan with new tax-deductible contributions. If you have active self-employment income, this is the quickest and easiest way to fund your Solo 401k.

3) Locate the Property

If you already have a property in mind, then you’re all set! If you don’t yet have a turnkey passive cashflow deal maker, you’re in good hands. At Solo 401k, we provide resources like dealmaker access to our Solo 401k accountholders so that finding a profitable deal is easy.

As your Solo 401k document provider, we don’t sell the investments ourselves, but we are happy to share what we’re doing with our Solo 401ks and give access to those resources to our accountholders. We believe in walking the walk, so we only refer our accountholders to dealmakers with whom we have invested personally or have done extensive due diligence.

After you have the property identified, you’ll put in your offer using the name of your Solo 401k Trust (e.g. John Doe 401k Trust). If there’s any earnest one to put down, you can write the check out directly from your Solo 401k bank account. Your Solo 401k will own the property, so you want to be sure to use only you Solo 401k funds to pay for any fees.

4) Offer and Closing

One of the great things about your Solo 401k is that you have flexibility in purchase methods.

This means you can pay for the property in full using your retirement funds (if no mortgage is needed/wanted) or you can get financing for your purchase. It’s possible to get a non-recourse loan for your Solo 401k to use leverage to purchase your property. Unlike the Self-Directed IRA (SDIRA), the Solo 401k is not subject to the Unrelated Debt Financing tax (UDFI). This makes the Solo 401k the easiest retirement vehicle available to use leverage purchasing a property.

In any offer documents and at the closing table, the Solo 401k itself is the buyer. This keeps the retirement funds separate from you and keeps those funds tax-deferred. You are the trustee of your Solo 401k, so you sign the closing documents. The check presented at closing will be from your Solo 401k bank account. You’re in total control during the entire deal.

5) Fees and Other Aspects of Your Real Estate Deal

If you have any ongoing expenses, such as property taxes and/or maintenance for the property, they should be paid from your Solo 401k bank account. Remember that personal funds and retirement funds should never mix to avoid triggering prohibited transactions or a taxable event.

Say Good-bye to Bureaucracy and Hello to Freedom

As the pioneers of checkbook control, we paved the path for bureaucracy-free self-directed investing. In real estate a holding institution, such as a custodian, can create delays and red tape that can kill profitable deals before you get the profit. Instead of days or weeks of third party processing, we empower you to finalize deals with the ease of signing a check.

Governed by a special section of tax code, the Solo 401k by Nabers Group enables you to be your own custodian legally. Sacrifice nothing, compromise nothing, and gain the fast-mover advantage required of all successful real estate investors.